The One Health Plan Model That Doesn’t Win When You Lose

When It Comes to Paying for Healthcare, Incentives Aren’t Just a Detail—They’re Everything

I recently read a popular post leveling broad criticisms at employer-sponsored health plans. The assertions were familiar: claim delays, poor design, misaligned incentives, a system that fails the very people it’s supposed to protect.

Where’s the lie? None so far. Many employer plans are outdated. Most are clunky. Others are structured by brokers who benefit more from renewals than from results. And too often, they still lean on carriers—many of them owned by Wall Street or private equity—for administrative functions, networks, or both. That reliance quietly drags them back into the very models they’re trying to escape, reintroducing the same hidden fees, inflated markups, and perverse incentives they thought they’d left behind. But as I read through the arguments, something struck me: the entire critique, while not entirely wrong, felt overwhelmingly misguided.

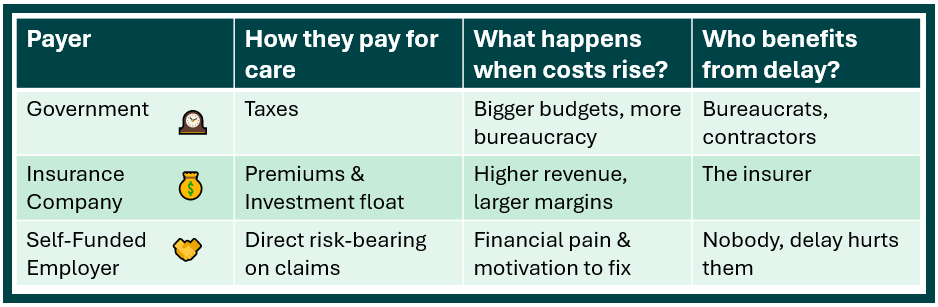

Why? Because it ignored a simple but essential reality—there are only three entities in the U.S. that ultimately pay for healthcare:

The government/taxpayer (via programs like Medicare, Medicaid, or the VA)

Insurance companies (as the actual payer in fully insured and individual-market plans)

Employers (when they self-fund and become the payer directly)

And among those three, the employer is—by far—the least conflicted and the most amenable to optimization.

So yes, criticize what needs improving. But let’s not pretend the playing field is even. Because it’s not.

Door One: Government Healthcare — Waste, Bloat, Bureaucracy

Government-run programs are never efficient and even less nimble. When Medicare or Medicaid allow claims to sit unresolved for months, or when provider reimbursements are mispriced and left to rot in regulatory gridlock, there’s no market consequence. Just more forms, more layers, more bureaucracy. I can’t help but think of the common claims made by auditors and investigators that one-third of all U.S. healthcare delivery is lost to waste, fraud and abuse. No other delivery mechanism is less efficient than the government.

These programs grow through inefficiency. Waste justifies budget increases. Delays create staffing needs. Complexity breeds control.

They’re not built to optimize—they’re built to expand.

Try navigating a Medicaid billing issue. Try appealing a Medicare overpayment clawback. It’s a Kafka novel with a fax machine.

Door Two: Insurance Carriers — Profit by Delay and Inflation

Commercial carriers, meanwhile, are playing an entirely different game—one that most plan members (and many employers) still don’t understand.

Under the Affordable Care Act’s Medical Loss Ratio (MLR) rule, insurers are limited to keeping 15–20% of premium dollars as revenue. But that limit is tied to a percentage. So as total claim costs rise, allowable profits rise with them.

They have no financial incentive to lower costs. On the contrary—they benefit when claims inflate. The bigger the claim, the bigger the premium next year.

What’s worse? They know they can better optimize this revenue source by delaying care. Every week they stall an authorization, every month they hold onto your premium dollars without paying claims, they earn interest, investment returns, and inflationary gains. It’s float on steroids.

They don’t need to deny care outright. They just need to slow it down. And, in the meantime, your health suffers while their earnings grow.

Door Three: Employers — Incentivized to Get It Right

Now compare that with employers who self-fund their plans. When an employer acts as the payer, inflated claims hit their own ledger—not some insurer’s balance sheet.

That changes everything.

Employers lose when employees get sicker. They win when employees are well, productive, and present. That incentive structure—while often underleveraged—is fundamentally aligned with what we should want from a healthcare financing model.

They’re also the only payer flexible enough to do something about it. Employers can break away from bloated PPO networks, ditch conflicted pharmacy contracts, and invest in models like Direct Primary Care or surgical bundles that actually lower costs and improve outcomes.

Are all employers doing that? Of course not. But they can. And increasingly, some are.

Missing the Forest for the Fees

So yes, we should point out when an employer-sponsored health plan underperforms. We should highlight poor design, wasteful vendors, or lazy advisors. But let’s not confuse a fixable flaw with a fundamental failure.

Because the alternative is a government system that grows stronger through waste, or a commercial insurance model that profits more the longer you wait and the worse your care gets.

Employer-sponsored plans aren’t perfect. But they’re the only model where the payer doesn’t win when you lose.

And in a system where every other player is actively monetizing delay, confusion, and chronic inefficiency—that matters.